MICRO-Finance Company Registration: SETTING UP A MICRO-FINANCE COMPANY

What Are Micro-Financing Institutions?

The government of India is working with full earnestness towards a major policy objective shift to achieve financial inclusivity. To fulfill this dream, the Microfinance Institutions have taken center stage as they extend financial services to people of low-income strata working tirelessly to find a way out of poverty.

Microfinance refers to an array of financial services, including loans, savings, and insurance, available to poor entrepreneurs and small business owners who have no collateral and wouldn’t otherwise qualify for a standard bank loan. More often, small loans are given to those living in developing countries and working in small businesses of different trades like carpentry, fishing, transportation, etc.

India is a growing economy with a large population. Government banks and private sector banks cannot open their branches in every village. Though Indian banks have increased their presence but still they have limited reach in remote areas. Micro Finance Company Registration allows these financial institutions to work in remote areas and empower farmers or small businesses in the villages.

Basic Features of a Micro-Financing Institution

With micro finance company registration, a small finance institution can be introduced in a rural or remote area with an objective to assist the unbanked and under-banked sections of the Indian population. Over the years, microfinancing has emerged as a unique economic development tool that has helped crores of underprivileged people.

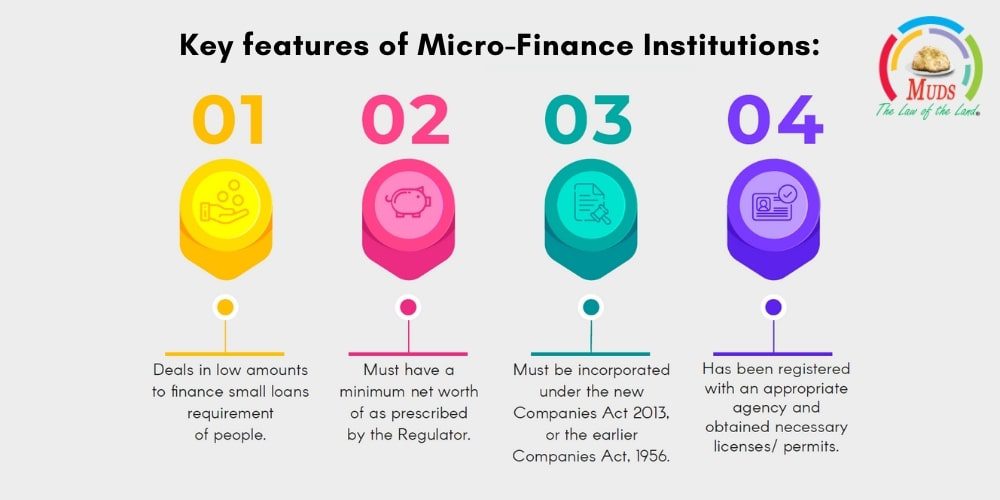

Following are the key features of Micro-Finance Institutions:

- Deals in low amounts to finance small loans requirement of people.

- Must have a minimum net worth as prescribed by the Regulator.

- Must be incorporated under the new Companies Act 2013, or the earlier Companies Act, 1956.

- Has been registered with an appropriate agency and obtained necessary licenses/ permits.

Benefits of Micro-financial Business

The distinctive features of the micro-finance lending management solution allow lenders to have access to this huge untapped sector of the Indian economy without the need for manual intervention, excessive paper load, and massive wait times.

Governments of India and the Reserve Bank of India have created a conducive policy framework for Microfinance Institutions (MFIs) to ensure legitimacy and impetus to the sector.

The following are the benefits of getting Micro Finance Company Registration:

- Provides access to funding for small businesses.

- Encourage self-sufficiency and entrepreneurship among the rural population.

- It offers a better overall loan repayment rate than traditional banking products.

- Strengthen the financial condition of businesses or people requiring instant capital.

- Helps in meeting credit needs for such a population range by offering various loans like emergency loans, consumption loans, business loans, working capital loans, housing, etc.

Different Categories of Micro-Finance Companies

Microfinance can be broadly categorized into 3 types, based on type of products:

a) Micro-loans –Microfinance loans are significantly different from others as these are provided to borrowers without any collateral. The aim of these small loans is to have its recipients outgrow smaller loans and be ready for traditional bank loans.

b) Micro-savings – Micro-savings accounts are a unique concept as they allow entrepreneurs to operate savings accounts with no minimum balance. The main objective of such accounts is to help users inculcate financial discipline and develop a habit of saving for the future.

c) Micro-insurance– Micro-insurance is a uniquely designed insurance cover provided to borrowers of microloans and its distinct feature is that these insurance plans have much lower premiums than traditional insurance policies.

Brief About Micro Finance Business

Micro Finance Institutions (MFIs) in India have played a major role in its overall development, as these institutions have empowered underprivileged people by extending monetary support to all communities and regions. The MFIs have gained a foothold in rural areas and underdeveloped areas, where nationalized banks are yet to reach. Thus, by giving opportunities to millions of people to fulfill their dreams and ambitions, these MFIs not only help in the economic growth of the country but also in a fair distribution of wealth in all parts.

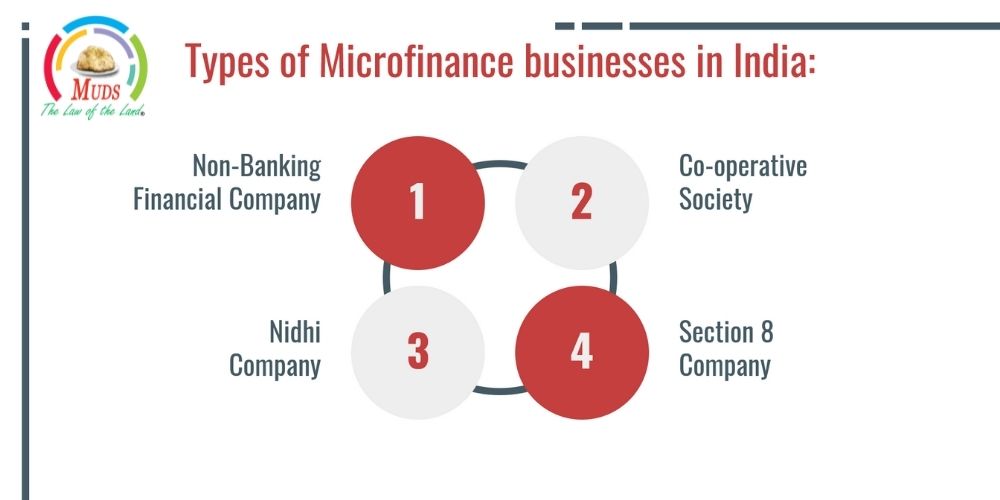

Listed below are few most prominent types of Microfinance businesses in India:

| Particulars | NBFC-MFI | Section 8 Companies | Cooperatives and Mutually aided cooperative societies | Societies and Trusts | Nidhi Company |

|---|---|---|---|---|---|

| Registration Under | Registered under Companies act 2013 and with Reserve Bank of India | Registered under Companies act 2013 | Multi-State Cooperative Societies Act, 2002 | Societies Registration Act, 1860 and/or Indian Trust Act 1882 | Registered under Companies act 2013 |

| Net Worth | Minimum net owned funds of 5 crores. For North Eastern requirement is 2 crore | No minimum requirement | No minimum requirement | No minimum requirement | No Minimum Capital Requirement |

| Recommended For | Poor and lower-income group | Non-Commercial Banking and NPO | Non-Commercial Banking and NPO | where members have a common interest | Poor and lower-income group |

| Rate of interest | (1) The average base rate of five largest commercial banks multiplied by 2.75 per annum

(2)cost of funds plus margin cap of 10% for MFIs having loan portfolio above ` 100 crores and 12% for those with loan portfolio less than 100 crore The lower of (1) and (2) |

Same as NBFC-MFI | Decided and Approved by the Board of Directors | Decide and approved by members at general meetings and by the committee | Maximum Rate of Interest on Loan = 7.5% + Maximum rate offered on deposits. |

-

Non-Banking Financial Company – Micro Finance Institution (NBFC-MFI)

Reserve Bank of India (RBI) defines NBFC-MFI as a non-deposit-taking company under NBFC micro finance company registration (other than a company licensed under Section 25 of the Indian Companies Act, 1956) with Minimum Net Owned Funds of Rs.5 crores.

For NBFC incorporation of MFIs in the North Eastern Region of the country, the Minimum Net Owned Funds specified is Rs. 2 crores.

All companies seeking micro finance company registration as NBFC-MFIs must have more than 85% of its net assets as “qualifying assets”.

NBFC – MFIs must fulfill the following criteria for NBFC Micro finance company registration:

- Loan disbursed by an NBFC-MFI to a borrower with a rural household annual income not exceeding 1,00,000 or urban and semi-urban household income not exceeding 1,60,000;

- The loan amount does not exceed 50,000 in the first cycle and 1,00,000 in subsequent cycles;

- The total indebtedness of the borrower does not exceed 1,00,000;

- Tenure of the loan should not be less than 24 months for loan amount in excess of 15,000 with prepayment without penalty;

- Loan to be extended without collateral;

- The aggregate amount of loans, given for income generation, is not less than 50 per cent of the total loans given by the MFIs;

- The loan is repayable on weekly, fortnightly or monthly installments at the choice of the borrower.

NBFC Micro Finance Company Registration Procedure in India

NBFC Micro finance company registration procedure in India to be followed is according to the guidelines specified by the RBI.

Step 1: Register a Company

Step 2: Raise authorized and paid-up capital to Rs.2 crore

Step 3: Deposit Rs.2 crore in fixed deposits and obtain a certificate

Step 4: Get all the certified copies and complete the other RBI formalities

Step 5: Fill online application for micro finance company registration

Step 6: Submit the hard copy of the application for micro finance company registration to the Regional Office of the RBI

After the completion of the NBFC Micro finance company registration procedure in India, the Head Office of RBI shall issue the NBFC license. An applicant can check the status of the application online with the help of acknowledgment number.

-

A Section 8 Company:

Section 8 Company is a company registered under the Companies Act, 2013 for charitable or not-for-profit purposes, which pertains to an established ‘for promoting

- Commerce

- Art

- Science

- Sports

- Education

- Research

- Social Welfare

- Religion

- Charity

- Protection of environment

- Or any such other object’, provided the profits, if any, or other income is applied for promoting only the objects of the company and no dividend is paid to its members.

Registration through Section 8

Compared to NBFC-MFI, the requirements for registration of a section 8 Company and apply for central government licenses is quite simple.

Requirements for Registration Under Section 8

Maximum INR 50,000 can be given for the business purpose and INR 125,000 for the residential dwelling.

- No minimum net owned fund requirement.

- No RBI approval is required since RBI has exempted such companies from registration.

-

Nidhi Company:

A Nidhi is a company that seeks micro finance company registered under Section 406 of Companies Act, 2013 and is classified as an NBFC.

“Nidhi” means a company that has been incorporated as a Nidhi with the object of cultivating the habit of thrift and savings amongst its members, receiving deposits from, and lending to, its members only, for their mutual benefit.

The deposits, thus gathered in a Nidhi company are then used for its members or shareholders and the company provides loans or advances, acquires government-issued stocks, bonds, debentures, securities, etc.

A micro finance company registration done as a Nidhi company is regulated by the Ministry of Corporate Affairs and all its financial dealings are monitored by the RBI.

-

Co-operative Society:

A micro finance company registration of a Cooperative Society is done as that of an autonomous association of people united voluntarily to meet their common economic, social, and cultural needs and aspirations through a jointly-owned and democratically controlled business. Thus, cooperatives cannot accept deposits from the general public but are only permitted to do so through their members.

When cooperatives and microfinance go hand in hand and are managed well, as registered under micro finance company registration, then they render help and power to the neediest and help improve their lives.

Cooperatives seeking micro finance company registration are to be done under the conventional state-level cooperative acts, the national level Multi-State Cooperative Societies Act (MSCA 2002), or under the new State-level Mutually Aided Cooperative Societies Act (MACS Act).

FURTHER MICRO FINANCE BUSINESS CAN FURTHER BE CLASSIFIED AS:

- Payday loan business online

- Peer to Peer (P2p) Lending

(a) Payday Loan Business Online:

Payday loans have grown in popularity over the years, mainly as a result of the economic downturn and tightening lending practices by banks and credit unions. Many individuals who previously could get approved for a personal loan or borrow against the equity in their homes have found that they no longer qualify for these types of loans.

Payday loans are short-term loans that require no collateral and generally range in amounts from 5000 to 50000. They are meant to be fully repaid within a very short period of time (two weeks). Lenders provide these loans to consumers who are faced with an unexpected financial situation that can’t be put off until the next time they get paid.

A payday loan is a unique and practical concept under which small, unsecured short-term cash loans can be borrowed by people to get through the month until their next salary comes in hand.

Typically, Payday loans target the working classes who have difficulty in making two ends meet at the end of each month and these loans need to be repaid within a short period of time. These loans come at a very high cost due to short tenure, urgent nature, and repayment risk associated with it. Payday loans in India are availed by people only in case of an emergency like a medical emergency, wedding, payment of school fees, etc.

(b) Peer to Peer (P2P) Lending:

P2P lending is a form of crowd-funding used to raise loans that are paid back with interest. It can be defined as the use of an online platform that matches lenders with borrowers in order to provide unsecured loans. The borrower can either be an individual or a legal person requiring a loan. The interest rate may be set by the platform or by mutual agreement between the borrower and the lender. Fees are paid to the platform by both the lender as well as the borrower.

The borrowers pay an origination fee (either a flat rate fee or as a percentage of the loan amount raised) according to their risk category. The lenders, depending on the terms of the platform, have to pay an administration fee and an additional fee if they choose to use any additional service (e.g. legal advice etc.), which the platform may provide.

P2P lending works very differently from other financing tools and borrowing from these is not from a financial institution but it is from an individual or group of individuals who are willing to loan money to applicants who are found qualified as per the criteria set by them.

BRIEF PROCEDURE REQUIRED TO BE FOLLOWED FOR SET-UP MICROFINANCE BUSINESS

Step-1 The Applicant Company must comply with the registration requirement under the new Companies Act 2013/ Reserve Bank of India/ Multi-State Cooperative Societies Act, 2002/ Societies Registration Act, 1860 and/or Indian Trust Act 1882.

Step-2 The applicant company must have sufficient net worth according to the micro finance business requirement.

Step-3 Determine your risk-bearing capacity and structure your business.

Step-4 Apply for registration with the regulation agency and obtain the necessary permits/licenses.

Step-5 After satisfaction of all requirements the regulation agency will grant a registration certificate and necessary permits/license as the case may be.

It was rightly said by Ralph Waldo Emerson– “Every Wall is a Door”

Thus, take a step forward to open the door for the new FDI norms.

MUDS MANAGEMENT is recognized as one of the most-respected, knowledgeable, and pocket-friendly legal and financial solutions company. Give us a call right now at +91 9599653306 and start a conversation immediately for Micro Finance Company Registration.