Recovery of Debts by Financial Creditors

The Insolvency and the Bankruptcy Code was drafted and enacted to consolidate and amend the laws in relation to reorganization and insolvency resolution of Corporate Persons, Individuals, and Partnership Firms. It is evident to highlight that in the preliminarily phase only the provisions related to corporate persons were notified. The provisions related to individuals and partnership firms are yet to be notified. The main emphasis of the code was on creating and aligning in place time-bound processes thereby leading to maximization of value of assets of the aforementioned, promotion of entrepreneurship, availability of credit along with balancing the interest of all the stakeholders.

The Insolvency and Bankruptcy Code in its early stage repealed the already existing legislations which had become outdated with the passage of time. The Code is not an easy legislation as the drafters of the legislation burned the mid night oil to create a masterpiece legislation that would cater to the solve the issues of the society. The Code is detailed and elongated covering numerous time bound processes designed for the persons covered under the applicability of the code.

On this note the Section 3 and Section 5 of the Code defines numerous terms which are of high importance and relevant for interpretation of the code. Without having a glance at the section 3& 5 of the code it would be cumbersome to analyse and interpret the provisions of the code. Under the section 3 &5 of the code numerous terms have been crisply defined with reference and inline to the Insolvency and Bankruptcy Code.

As per the Code the term debt means an obligation or a liability in relation to a claim which is due from any person. A special contribution and value addition made by the Code is that under the code for the first time the bifurcation of the term debt has been made very priestly.

On this note under the Code the debt has been bifurcated into financial debt and operational debt.

The term financial debt as enshrined in the code meant a debt along with interest (if any) which is to be disbursed against the consideration for the time value of money. The definition of financial debt included within its ambit an inclusive list of items which fell within the purview of financial debt. In line to this definition the financial creditor meant to be a person to whom a financial debt as above defined was owed and also included a person to whom such debt had been legally transferred or assigned.

Operational debt means a claim in relation to provision or supply of goods or services thereby covering within its scope employment dues and statutory dues that are payable to the Central or State Government or any local authority under any law for the time being in force. Thereafter keeping the definition of operational debt into purview the operation creditors were defined to be persons to whom financial debt was owed and also included within its ambit persons to whom such debt had been legally assigned or transferred.

A remarkable fact to highlight is that the Insolvency and Bankruptcy Code in a very lucrative and lucid manner bifurcated the term debt into financial and operational debt. Another outstanding and praiseworthy fact incorporated under the Code was that the code introduced a new class of creditors by classifying the creditors on the basis of debt into financial and operational creditors. This was the first time that the creditors had officially been classified on the basis of debt apart from the classification on the basis of security into secured and unsecured creditors.

In this article we will mainly direct our focus towards recovery of bad debts by financial creditors.

Financial creditors as already discussed are persons to whom a financial debt is owed. Also the term financial creditor covers within its purview persons to whom such debt has been legally transferred or aligned. Therefore all lenders who have extended any kind of loans, guarantees or financial credits are covered within the scope and ambit of financial creditors.

On 6th June 2018 a major amendment came in the favor of the financial creditors in the form of Insolvency and Bankruptcy Code (Amendment) Ordinance 2018. Through the amendment the home buyers and allottees under the Real estate (Regulation and Development) Act 2016 got the status of financial creditors under the Insolvency and Bankruptcy Code. The positive effect of the amendment was that the home buyers and other allottees were able to invoke section 7 against the defaulting promoters. Prior to the amendment the home buyers were treated as unsecured creditors. The amendment is a big relief for the homebuyers.

After having discussed and interpreted as to who financial creditors are, we will now head toward discussing the recovery modes and mechanism available with these financial creditors.

The financial creditors occupy the supreme position and ranking under the code. They have priority and say on all matters that are covered and elaborated under the code. They have been bestowed with voting rights and majority stake during the course of constitution of the committee of creditors. Also the financial creditors enjoy privilege of being repaid on priority basis once the proceeds are realized after the insolvency order is passed by NCLT. The biggest power that financial creditors hold with them is that in the scenario of default they can directly approach the NCLT for seeking the insolvency of the debtor concerned.

The data as Published by the IBBI states that out of 1858 cases that have been filed till date around 738 cases have been filed by the financial creditors. Out of the 738 cases filed 172 were filed during quarter ended 31 March 2019. The names of a few cases that were filed by the financial creditors are as follows:

- Venky Hi-Tech Ispat Ltd.,

- BSR Diagnostics Ltd.

- Sunil Ispat & Power Limited

- Alok Industries

- Essar Steel India Ltd.

- Dhanalaxmi Paper Mills Pvt. Ltd.

- Jyoti Structures Limited

Prerequisites for Debt Recovery via IBC

- The minimum amount of default to be recovered should be atleast one lakh rupees.

- The debt to be recovered should a debt that was due for recovery after December 2016.

- There should be evidences of written communications made in relation to the debt due to be recovered.

- There should be proper copy of agreements and deeds that were entered as evidence in support to highlight the pending debt.

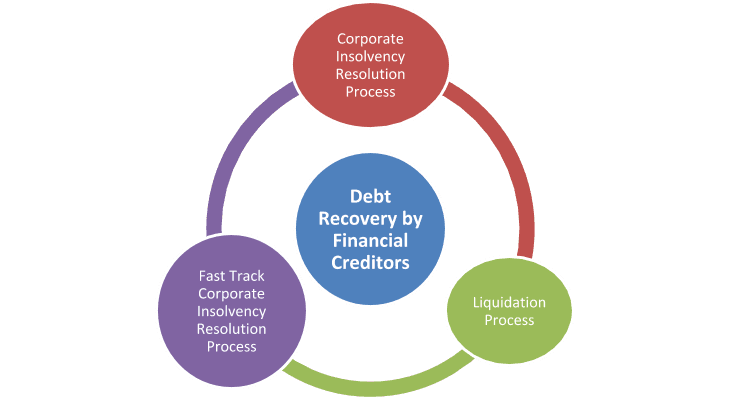

In light of the above the financial creditors may inorder to recover their debts initiate the below mentioned process via which they can recover their pending debts. The processes with the aid of which the financial creditors can recover their debts are as follows:

- By initiating the Corporate Insolvency Irresolution Process (CIRP)

- By taking shelter of Liquidation Process

- By taking recourse of Fast Track Corporate Insolvency resolution Process (FTCIRP)

Corporate Insolvency Resolution Process (CIRP)

On the occurrence or commitment of default by the corporate debtor, the financial creditors can either individually or jointly with other financial creditors file an application to commence the insolvency proceedings against the defaulting corporate debtor.

The financial creditors have the sole privilege of directly approaching the NCLT for filing the application in relation to initiation of corporate insolvency resolution process. They are not required to prove their debts forth the NCLT prior to submission of application for insolvency resolution process. They are granted the express authority to directly knock the doors of the NCLT for recovery of their debts from the defaulting corporate debtors.

On this note the financial creditors are required to make an application in Form 1 along with a fee of Rs. 25,000. The financial creditors while filling the application for initiating the corporate insolvency resolution process as per section 7 of the code shall annex the following documents along the application that is to be submitted:

- The evidences of default as highlighted from the records as maintained by the information utility.

- The proposed name of the insolvency professional who would act as the interim resolution professional.

- Any other documents or evidences as highlighted by the IBBI.

Once the application is submitted by the financial creditors the same is reviewed by NCLT. The NCLT during the course of reviewing the submitted application ascertains on its own level the existence and nature of default that is highlighted by the financial creditor in the submitted application. It is significant to highlight that the NCLT reviews the submitted application within a time span of fourteen days from the receipt of application. After reviewing the received application the NCLT has the option of accepting or rejecting the received application. In the scenario where the NCLT opts to reject the received application then in such a situation it shall issue a notice to the financial creditor thereby giving opportunity to rectify the highlighted defects.

Once the application is admitted by the NCLT then the corporate insolvency resolution process is deemed to have commenced from the very date on which the application for corporate insolvency resolution process was accepted by the NCLT.

After having arrived at the decision of accepting or rejecting the received application the NCLT shall convey its decision via an order to the financial creditor and corporate debtor if it accepts the received application and to the financial creditor only if it rejects the submitted application.

A crucial fact to be kept in purview is that the Code has prescribed the time line of one hundred and eighty days within which the entire process of corporate insolvency resolution process needs to be completed. The appointed resolution professional shall make his best endeavors to complete the entire process within the prescribed time line of one hundred and eighty days. Even after making the best efforts to complete the process within due time if the process remains uncompleted the in such state the resolution professional may approach the NCLT for seeking extension in time frame to complete the ongoing process. The maximum extension that may be granted by the NCLT for completing the ongoing process is ninety days. It is important to note that the extension in time frame shall be granted only once by the NCLT.

Thus the first step in the direction of debt recovery by the financial creditors is to initiate the corporate insolvency resolution process against the defaulting corporate debtor. If due to any reasons the process of corporate insolvency resolution process does not yield the desired results then the financial creditors may take the next recourse of initiating the liquidation process against the defaulting corporate debtor.

Liquidation Process

In the scenarios where the NCLT does not receive a proper resolution plan or it rejects the received resolution plan on account of non-compliance with the specified requirements then in such cases the NCLT concerned may pass orders for liquidation of the concerned corporate debtor along with issuing a public announcement for the same and forwarding the copy of aforesaid order to the concerned ROC with which the corporate debtor is registered.

The resolution professional as appointed during the course of the corporate insolvency resolution process may with the approval of the committee of creditors request the NCLT to liquidate the defaulting corporate debtor. On receipt of the aforesaid request from the resolution professional the NCLT shall after requisite review pass the order for liquidation of the defaulting corporate debtor.

It is important to note that once liquidation order has been passed by the NCLT then in such a scenario no fresh suit or legal proceeding shall be initiated or filed by or against the concerned defaulting corporate debtor. If required the appointed resolution professional may initiate any suit or legal proceeding with the express approval of the NCLT.

Once the liquidation order is passed by the NCLT against the defaulting corporate debtor the order passed will act as a discharge notice after which the officers, employees and workmen of the corporate debtor will have to relinquish their job. The officers, employees and workmen of the corporate debtor shall continue to work in the scenario where the business of the defaulting corporate debtor is kept running and in operation by the liquidator during the course of the ongoing liquidation process.

It is evident to note that the resolution professional as initially appointed at the time of the corporate insolvency resolution process shall act as liquidator to carry forward the liquidation process. After the appointment of liquidator the board of directors, key managerial persons and partners of the defaulting corporate debtor shall have no role in the business and their respective powers shall move towards the liquidator. Therefore the liquidator will be the main controller of the business of the defaulting corporate debtor during the course of the liquidation process.

The liquidator apart from managing and looking after the business of the defaulting corporate debtor shall form a liquidation estate comprising of the assets of the corporate debtor. The liquidator during the course of forming the liquidation estate shall stand in the position of fiduciary in relation to the liquidation estate thereby keeping the interest of the creditors in safe and secure.

Fast Track Corporate Insolvency Resolution Process

An application for initiating the fast track corporate insolvency resolution process may be made by the financial creditors against the defaulting corporate debtor. The application for fast track corporate insolvency resolution process may be made by the financial creditors against the following:

- Small company- As defined under the Companies Act 2013

- Startups – As defined in the Government of India notification dated 23rd May 2017 as issued by the Ministry of Commerce & Industry.

- Unlisted Company – Companies having total assets not exceeding one crore as reported in the financial statements of the immediately preceding financial year.

The Code has prescribed a time span of ninety days within which the entire process of fast track corporate insolvency resolution process needs be completed .Even if after the best endeavors the process of fast track corporate insolvency resolution process remains incomplete then in such a scenario the appointed resolution professional may file an application to NCLT for extension of timeline to complete the ongoing process. On receiving the application for extension of time line for completing the ongoing fast track corporate insolvency resolution process if the NCLT is satisfied that the ongoing fast track corporate insolvency resolution process is such that it cannot be completed in the prescribed time line then in such case the NCLT may extend the prescribed time line by a further duration not exceeding forty five days. E aforesaid extension in time frame shall be granted only once by the NCLT.

The financial creditors for initiating the fast track corporate insolvency resolution process shall file an application to the NCLT thereby attaching the requisite documents along with the application. The set of documents that need to be attached with the application are as follows:

- Records as maintained by the information utility highlighting the default committed by the corporate debtor

- Any other document as required by the IBBI to suffice that the defaulting corporate debtor against whom application is filed is eligible for fast track corporate insolvency resolution process.

The fast track corporate insolvency resolution process is a shorter version of the corporate insolvency resolution process. The process flow is same but the difference is in the timelines as in case of fast track corporate insolvency the prescribed timeline is just half as compared to the corporate insolvency resolution process.

Therefore the debt recovery under the Insolvency and Bankruptcy may be time consuming but the processes are result oriented in terms of providing the desired outcome. The financial creditors need to be patient and trust the process flow via which they would be successful in recovering their debts. The code is on the track of getting the pending debts recovered, it’s just that right recourse needs to be adopted to do the needful. The banks and financial institutors have successfully recovered their NPAs and stressful assets via the processes as enshrined in the Code.

Hope this article was informative in providing the debt recovery alternatives available with the financial creditors.

Stay connected with MUDS for updates